// We must be exceptionally careful while diagnosing and treating the current inflation

I

nflation has reached the peak point for many countries across the globe in the last 40 to 100 years. Most countries consider it a major problem because there is no way to know whether inflation has passed the pinnacle. Experts continue to debate. If inflation continues to grow, grave socio-economic problems will become inevitable in the entire world. The policies central banks choose to curb inflation are like playing with fire: no margin for error. A slightest mistake can lead to more serious consequences. How did the world come to this point? When the pandemic hit in 2020, the cash balances of the US and the European central banks were at an all-time high. The volume of dollars and euros in circulation had increased twofold as a result of the quantitative easing policy, implemented by the FED (Federal Reserve System) and the ECB (European Central Bank) to save the economy after the 2008 crisis.

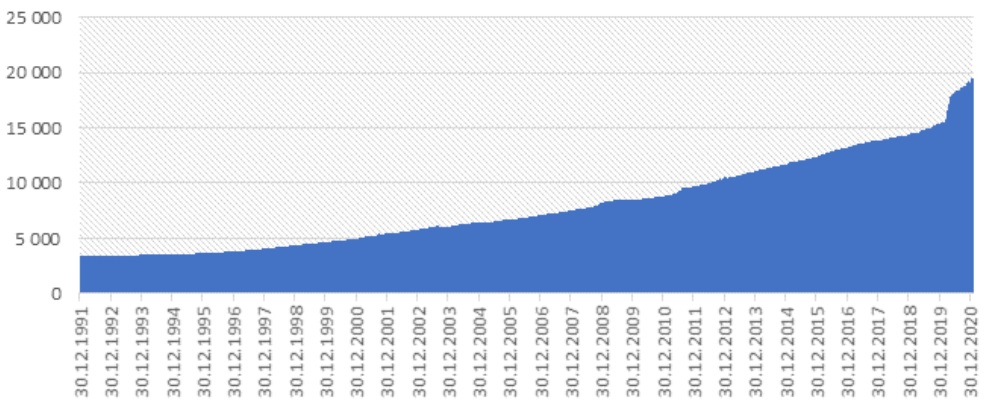

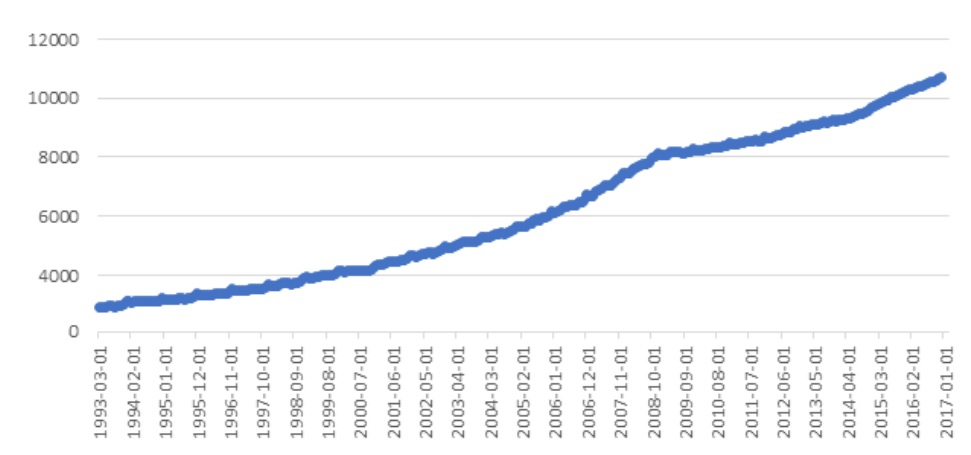

Everyone will remember the second decade of the 21 st century with the implementation of the same monetary policy under the motto of ‘continuing to treat the crisis’ . The ECB began to actively buy bonds of the Eurozone countries as of 2015. They tried to resuscitate the economy and boost the low inflation into the target level of 2 percent. The bank believed that the inflation that fluctuated around 1.5% was not enough to encourage economic activity. The ECB has spent almost 2.6 trillion euros over almost four years, from 2015 through 2018, buying up European bonds. In fact, it was a duplication of the policy the FED pursued in the USA, albeit with minor changes . The graphs below show how the money supply in the United States and the European Union has grown as a result of such monetary policy.

Money supply growth dynamics in the USA

The successive financial crises that hit the world (Russia in 1997, Brazil in 2000, Argentina in 2002, the USA in 2008) have cemented the positions of the central banks and boosted their roles. The concept of central banks that pursue independent policies have become a universal recipe. However, practice has repeatedly confirmed how wrong this approach has been.

Money supply growth dynamics in the Eurozone

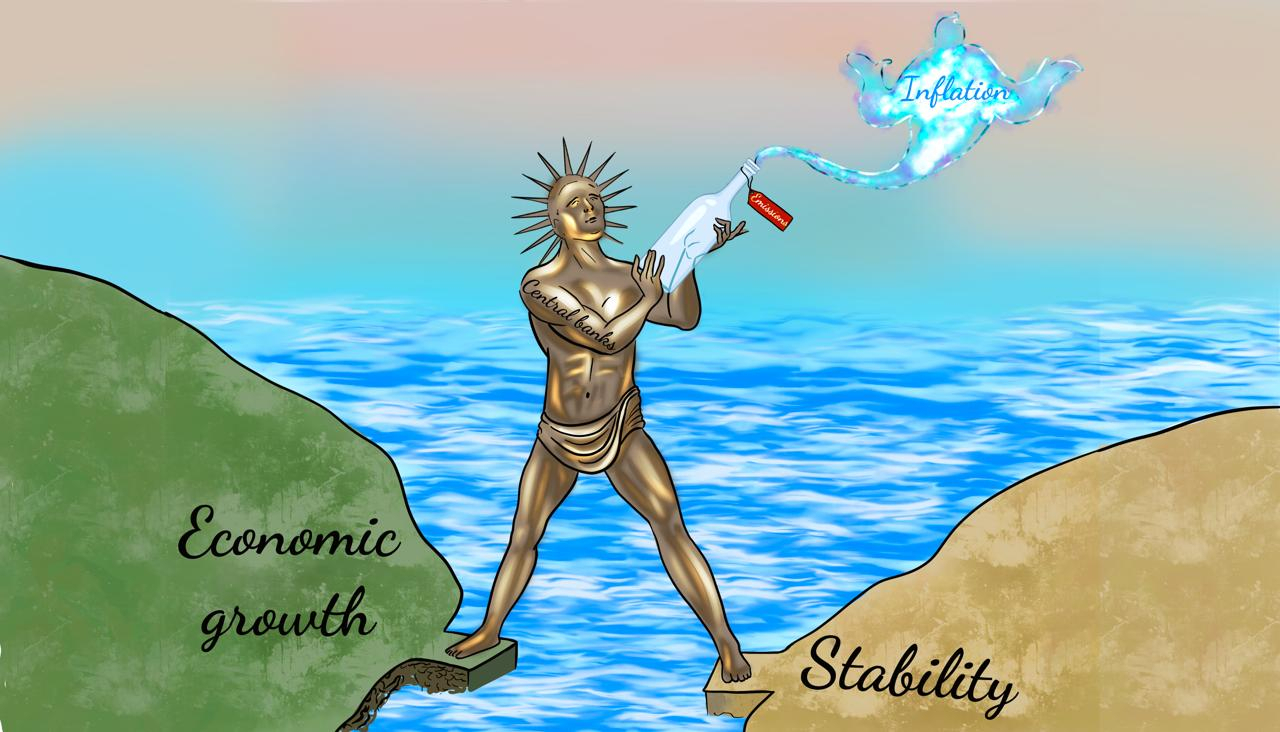

The modern-day world does not allow the classical scheme of circulating money supply backed by gold. When the overall GDP in the world was 83,885 billion dollars in 2020, the gold reserves stood at only 7,500 billion USD. Producing money at a situation like this requires a jeweller’s precision. If central banks fail to direct the money emission into the real sector as credit, it will create ‘financial bubbles’, leading to consequent crises and hyperinflation, instead of reviving the economy.

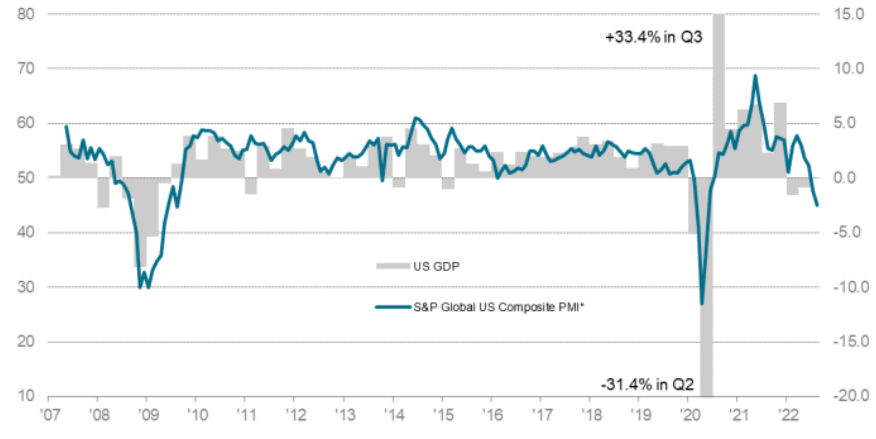

In a scenario like that removing that money from circulation will be even more troublesome. When a country records a lower GDP, the money supply in circulation must be reduced, but only through withdrawing credit invested into the economy. Following these interests, when central banks raise interest rates, loans become less available, which reduces economic activity, which then leads to bigger unemployment and social issues. If they choose not to act upon it, inflation continues to grow at a steep rate. The central banks then topple as the legendary Colossus of Rhodes. However, the similarity does not stop there: just like the Colossus, the central banks may look gargantuan from afar, but indeed have feet of clay. Diagnosing the inflation Central banks in 75% of countries followed by the International Monetary Fund have raised interest rates in response to rising inflation. Both the US Federal Reserve System and the European Central Bank have followed this course, tightening their monetary policy. It may be a standard reaction, but there is a flip side to the coin: More expensive loans inevitably reduce business activity, which may in turn lead to regression. S&P Global which measures business activity in the world has already recorded the lowest global PMI index in the last two years. A report by Oxford Economics shows that the probability of recession in the next 12 months in the USA and the EU has approached 60%.

The tight monetary policy pursued by central banks has reduced business activity to a 27-month low globally

Professor of Economics Elshad Mammadov, a recent guest at AzVision.az videocast project, says central banks bear great responsibility in this situation. An efficient monetary policy by central banks can create favourable conditions to build manageable parameters for the development of inflation. But their decisions should by no means be universal. Diagnosing the causes of inflation and determining its structure are the most important factors for an adequate monetary policy. Only then can they ‘prescribe a treatment’.

Elshad Mammadov: ‘We must first diagnose the inflation, and then choose an adequate monetary policy’

Its structure might consist of supply-side and demand-pull inflations. In some cases, both might overlap, overcomplicating the situation. The demand-pull inflation basically arises because of excess money supply in circulation. Currently the world has more than enough reasons for a demand-pull inflation. Demand-pull Inflation Several states adopted fiscal packages during the pandemic, which certainly caused currency, particularly dollar-euro bubble in the global market. In fact, since 2008 central banks who play a leading role in global economy, have been pursuing the policy of combating the economic crisis through considerably increasing the money supply. The short-term positive effect of such policy led to an economic revival and solution of certain economic problems. However, all these problems made an acuter comeback, which we are all currently experiencing globally. Some experts argue that around 70-80% of the growing money supply have gone to financial bubbles, instead of investments, which, rather than solving, further aggravated the existing economic problems.

Around 70-80% of the increased money supply during pandemic went to ‘financial bubbles’ instead of investments

Meanwhile, pandemic-related reasons are not the only causes of these ‘bubbles’. Economist Elman Sadigov clarified some of the hidden reasons that amplify monetary inflation in the world in his video interview to Azvision.az. He believes one of such reasons has to do with the policy of shifting to alternative energy.

Supporters of alternative energy and the traditional sources have been in disputes for years. But the advocates of alternative energy won last year, and they now must spend up to a hundred trillion dollars to implement their projects until 2040. The 3.1-trillion-budget of the US Federal Reserve System (FED) did not suffice to release this much money. FED had to increase the budget, so it did and should continue doing so. In any case, they have hit pause for the time being.

Elman Sadigov: ‘A recipe applied in one country cannot be blindly copied in another’

The tactics for combating ‘demand-pull’ (monetary) inflation might look obvious at first glance: If there is excess money in circulation, it must be reduced , which is why central banks in developed countries have launched tight monetary policies. However, the same policy might backfire, should other countries try to apply the same strategy. There are various subtleties to a monetary policy. The drivers behind the economies are also different. Some countries are resource-oriented, whereas others focus on export. The monetary policies pursued by export-oriented countries are completely different from those implemented in import-focused states.

Countries, whose money is also the reserve currency of the world, can issue as much money as they want, borrow comfortably, and not be exposed to the risk of exchange rate differences. A country like the US has a zero-devaluation risk, because their currency is the dollar. But many other countries must deal with devaluation risk , which means their currency faces a threat of losing value against the reserve currencies of the world. This mainly depends on the situation in the balances of payments and trade.

Neither Europe nor China can apply the monetary policy pursued by the USA. Europe does not have the same scope for manoeuvring. China did try to pursue a policy similar to America’s in 2008 to 2013, but could not yield the same results, because it had different problems. If the nature, content, and structure of inflation are not related to excess money supply in circulation, withdrawal of cash from economy can backfire majorly.

The US monetary policy is not suitable for others

All these arguments allow us to assume that there are currently no universal recipes. The institutions in charge must employ differentiated approaches, applying either restrictive or stimulating measures depending on the nature and content of the inflation.

We must also consider another crucial nuance: the inflation that has invaded the globe is not solely of monetary character. It is quite intricate in terms of structure, content, and character. It also includes supply-side aspects, meaning factors such as price hikes for fuel and food and disruption of logistics chains play a great deal in its structure. In other words, even if some magic wand were to cast all the excess money-supply out of the circulation and burst the ‘money bubbles’ by tomorrow, the prices would not quit rising. Approaches, ways out and management mechanisms should at least be as deep and diversified as the complexity of inflation. Supply-side inflation: The Three Heads of the Dragon There is a trio that especially stands out among the non-monetary causes behind the inflation: Rising fuel prices, tension in the food market and disruption of logistics chains.

Although we have been seeing a certain decline in oil prices, experts believe that to be a correction and prices to return within the $100-125 range by the end of the year. The International Energy Agency has grounds to expect the demand for oil to continue growing. The price for gas demonstrates a steady growth trend, dictated by geopolitical reasons, and many do not doubt that it will exceed $3,000 by the end of the year.

The Russia-Ukraine war is not the only factor that aggravates the situation in the food market. The drought that has hit Europe and agricultural policies pursued by some countries complement the long list. The protests of Dutch farmers against the government policy have become an endless series for over two months. The governments in Europe are caught between two fires: climate activists and farmers. Farmer protests are increasingly becoming a recurring trend in France, Italy, and several other countries.

The never-ending farmers’ protests in Europe are among the triggers of supply-side inflation

The UNCTAD (United Nations Conference on Trade and Development) reports that the third major challenge, the disruption of supply chains , is here to stay with us at least until late 2022. Although the boost in global transport-logistics costs and delays primarily affected the US, EU and British economies in 2021, the developing countries have been feeling the consequences in 2022 and will continue to do so.

Nijat Hajizadeh , head of department at the Centre for Analysis of Economic Reforms and Communication (CAERC), reminds that migrants comprised the majority of workforce in logistics and transportation companies in the United States and the Eurozone. Those migrants returning to their home countries or resorting to other fields altogether became one of the reasons behind price booms and delays in the logistics chains. Delays in supply chains increase production costs because Eurozone no longer has widely diversified expectations for raw materials. The growth of fuel prices also increases the costs for logistics services.

Nijat Hajizadeh: ‘WTO statistics show that the application of non-tariff barriers in 2021 has grown about 2.5-fold compared to 2019’

In the last 3 years, loading containers takes twice as long, the costs for unloading have grown threefold . The costs for transporting a single container have increased by 5 . This factor plays a significant role in supply-side inflation. Ordinary people might not always think about it, but the UNCTAD reports that logistics troubles cause 5-times more problems in developing countries than in rich ones.

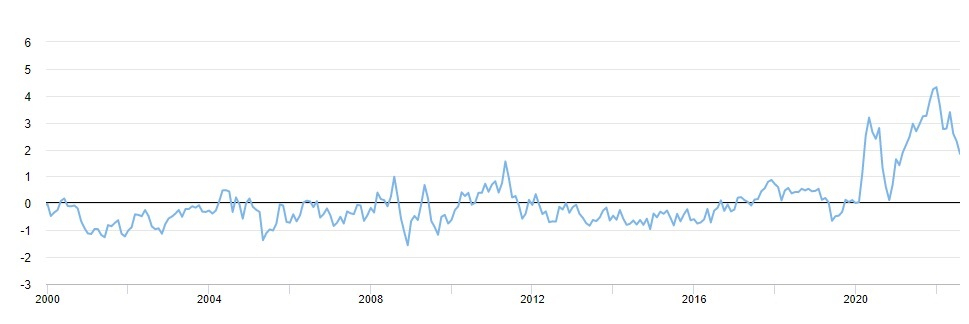

The GSCPI (Global Supply Chain Pressure Index) of the Federal Reserve Bank of New York has plunged slightly, however still remains above the optimal level of zero , at 2 points , which is a rather high indicator. Moreover, if any one of the expected risk scenarios (lockdown in China, escalation of tension around Taiwan, escalation of military operations in Ukraine, etc.) become a reality, the index will perform another leap up.

Although the Global Supply Chain Pressure Index has slightly decreased, it is still rather high

Alp Arslan Imamgulu, a security and logistics expert, believes that being on the lookout for alternative routes becomes especially urgent at times like these. Increasing transit cargo through Azerbaijan over the Caspian Sea and introducing the Zangazur corridor as an option can ease the logistics stress on Eurasia to some extent.

Alp Arslan Imamgulu: ‘The ongoing global economic-political issues will decide the further direction of logistics costs’

Neighbourhood Policy Against Inflation

The central banks of all regional countries are hard at work choosing an optimal policy to curb the inflation. Stanislav Tkachenko, Doctor of Economics and Professor at St. Petersburg State University, says that although the aftermath of the February-April-2022 ‘inflation blast’ in Russia has relatively calmed down, it is still too to predict whether the measures taken by the Central Bank have been successful . The government is pressuring the Central Bank to cut the interest rates much faster to support industry. However, the Bank pays a lot of attention to the development of the stock market.

Aidarkhan Kusainov, former advisor to the chairman of the National Bank of Kazakhstan, believes that inflation targeting is the only way to effectively curb inflation. The National Bank of Kazakhstan is essentially not pursuing inflation targeting; inflation is only accelerating, and the country is trying to fight it through administrative methods. The prices are mostly controlled by the state.

Asan Akhmetzhan, Director at the Department of Information and Communications at the National Bank of Kazakhstan, told AzVision.az that annual inflation in Kazakhstan increased from 8.4% in the beginning of the year to 15.0% in July. Both external and internal factors have played a part. The National Bank of Kazakhstan continues the disinflationary monetary policy it began last year within the program of ensuring price stability. The base rate has been increased by 475 basis points from 9.75% to 14.5% since early 2022. Therefore, the bank will go on implementing a disinflationary monetary policy, following the principles of the inflation targeting regime.

The Central Bank of Azerbaijan has chosen not taking any drastic actions. The Board of Directors of the Bank decided on 29 July 2022 to keep unchanged the accounting rate at 7.75%, floor of the interest rate collar at 6.25%, cap at 9.25%. Experts employ different approaches regarding what monetary policy the Central Bank should pursue: a restrictive or a stimulating one. There is no excess money supply in the country, so there is no need for the Central Bank to apply restrictive monetary policy, since the inflation is imported. Such policy will produce adverse results, weakening economic activity as a result of reduced investments.

The Great Challenge

The UN calculates that every 1% increase in food prices means another 10 million people in poverty globally. The inflation blast we have been observing after the war in Ukraine has brought about 95 more million poor people on the planet.

Unfortunately, nothing can be done globally to solve this problem. There are no relevant international institutions commissioned to fight it. The policy of international financial institutions serves the development of a single global economic model based on one currency. However, it is still possible to find remedies on a regional scale.

For example, it is not only possible, but of utmost necessity to do the following:

✔️for neighbouring countries to establish sound regional logistics schemes among themselves; ✔️remove excess money supply in circulation and invest it into regionally significant projects; ✔️to build constructive cooperation among central banks.

The most effective measure against inflation may be strengthening local production in regional countries, which raises the need for cooperation on an entirely new level.

-1728294271.jpg)

-1680010126.jpg)