Standard calculations of a country’s real effective exchange rate (REER) ignore global value chains that spread production processes across countries. Taking this factor into account leads to more accurate REER calculations, which can have profound policy implications.

The real effective exchange rate (REER) may sound arcane to non-economists, but it is one of the most important international financial indices. The REER is a summary index that tracks the difference in the prices of goods produced by a country and its trading partners. Other things being equal, an increase in a country’s REER indicates a loss of trade competitiveness. And rising current-account imbalances are often associated with deviations in the REER from equilibrium values.

Given the REER’s importance for economic policy – in the current trade discussions between the United States and China, for example – central banks and international financial institutions devote considerable resources to calculating and analyzing it. But their methods have become outdated as global value chains (GVCs) become increasingly widespread. We therefore recently proposed a new REER calculation with Zhi Wang that addresses the current shortcomings.

Standard calculations of the REER by most central banks and statistical agencies assume that countries export only final goods. But GVCs spread the different stages of production among different countries. They can do so thanks to technological improvements, lower trade barriers, and the closer integration of emerging markets into the global economy. Ignoring this reality can lead to substantial mismeasurement of the REER, resulting in questionable policy inferences.

To see how the standard approach could be wrong, consider a hypothetical value chain for the production of smartphones. Suppose Japan manufactures the components and ships them to China, where the phones are assembled and exported globally as finished products. Traditional REER models would assume that Japan exports final goods to China, and that the two countries are competitors. A depreciation of the Japanese yen, therefore, would help Japan’s competitiveness and hurt that of China.

In this case, however, a weaker yen would lower the price of Japanese components, which may lead to lower prices and increased demand for Chinese phones – leading to an improvement in China’s competitiveness. This example shows that the standard REER calculation is getting not only the magnitude wrong, but also the direction of change.

Our proposed framework addresses these problems. It also provides REER measures for individual sectors within a country. This makes it possible to assess the competitiveness of different parts of the economy, and to determine which sectors are the main drivers of the overall REER.

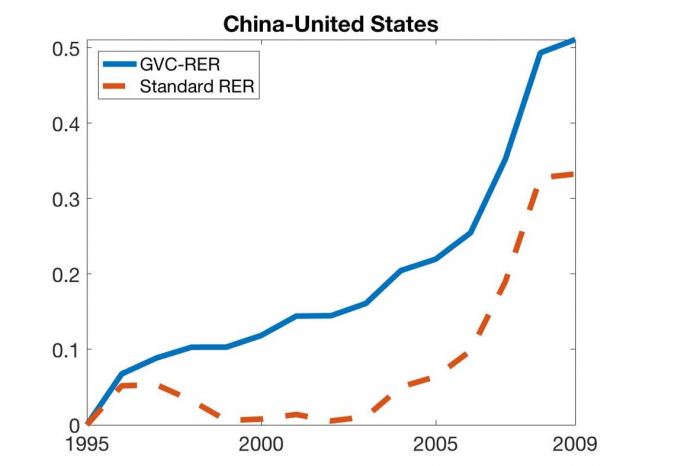

Taking GVCs into account alters our understanding of China’s bilateral real exchange rate against the US dollar. China has increased its global trade footprint massively following its accession to the World Trade Organization in 2001. The US, meanwhile, has long blamed its rising current-account deficit on the renminbi’s allegedly undervalued exchange rate.

Although China’s gross exports to the US are sizeable, China operates largely “downstream” in several GVCs. This is exemplified in the production of smartphones and electronic goods. As a result, a large part of Chinese exports represents value added embedded in parts and components from other countries besides China – including a significant share coming from the US itself. Moreover, US competitiveness relative to China depends more on prices in tradable sectors such as electronics than on those in non-tradable parts of the economy, like real estate. But commonly used aggregate measures of the REER do not allow for these distinctions.

Once these factors are taken into account, our analysis shows that China’s real exchange rate against the US dollar displays a pronounced and consistent appreciation trend. By contrast, the standard calculation shows a real depreciation of the renminbi in the period leading up to China’s abandonment of its exchange-rate peg in 2005, and then an exchange-rate appreciation that is smaller than the traditionally measured one.

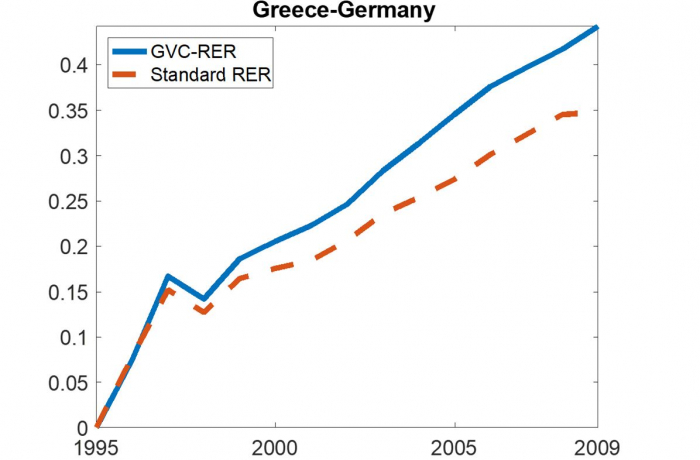

Similarly, for the eurozone, our GVC exchange-rate-based measure implies that Greece’s loss of competitiveness (or REER appreciation) relative to Germany was worse than the standard measure suggests, and that Greece’s competitiveness in the period leading up to the eurozone crisis was thus worse. This mismeasurement arose because the standard REER calculation was based on the extent to which Germany’s inflation rate differed from Greece’s, but it underestimated the difference made by GVCs.

Far from being a theoretical concept confined to economics textbooks, the REER has significant real-world relevance. Calculating it more accurately could reduce the risk of misguided economic policies. And it may lead policymakers to reach some very different conclusions about which measures to pursue.

Nikhil Patel is an economist at the Bank for International Settlements.

Shang-Jin Wei, a former Chief Economist of the Asian Development Bank, is Professor of Chinese Business and Economy and Professor of Finance and Economics at Columbia University.

Read the original article on project-syndicate.org.

More about:

-1780923278.jpg&h=190&w=280&zc=1&q=100)