Now, we may not be fans of the White House view that real growth is going to accelerate to 3% or more. Indeed, we remain of the view that the US economic recovery that began in 2009 is getting very mature. However, we doubt that the next recession will begin within the next few quarters, and despite some noise in the data due to the massive storms that hit this autumn, we can easily envisage growth remaining in the 2% range.

With real economic growth on a steady footing, and the White House desperate to enact some sort of tax reform, the US bond market is beginning to wake up to the potential that yields have been too low for too long. Chart 1 below shows the US 10 year generic bond yield. The increase in yield of 32 basis points since the nearby low in early September is the largest positive swing move of the year, and is threatening to breach a downward sloping trend line as indicated in the chart. The picture for the 5 year bond yield is similar, although that yield is now the highest in over 6 months.

Chart 1 – US 10 year Government Bond Yield

The main question in our minds is whether the recent move of 32 basis points, compared to the upward moves in April to May and June to July of 25 bps and 26 bps respectively, represents a subtle change in market character. If so, then should we look for higher yields over time? If not, then the recent move higher in yields probably stalls around about here.

Supporting the case for higher yields is 1) a continued shift away from ultra-easy monetary policies in the US, and to a lesser degree elsewhere, 2) expansionary fiscal policies in most developed countries, and 3) an expected increase in inflation in the US and Europe in the next couple of quarters or so which will only encourage central bankers to err on the hawkish side of expectations.

As for the Fed, they have told us that they are willing to look through soft data that has likely been impacted by recent storms. They are beginning to be worried that with the unemployment rate approaching 4%, the labour market is pretty tight and wage growth could accelerate. They are also content that inflation will move back to their 2% target, and they are modestly acknowledging that asset prices are high. Given all this, we suspect that they will continue to raise rates and reduce the balance sheet as they have previously outlined.

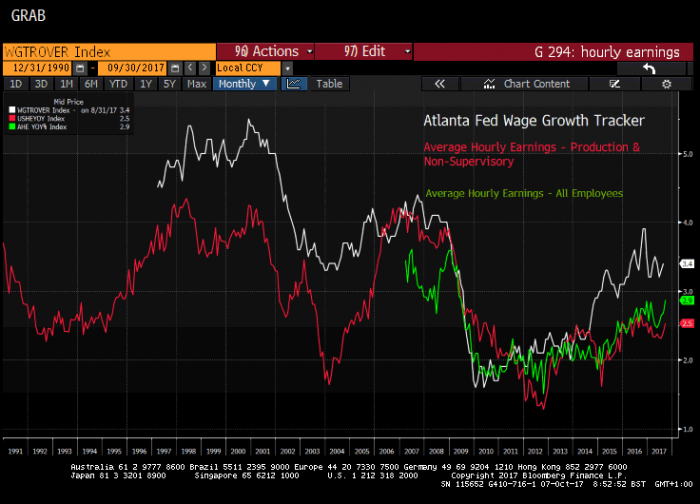

Arguably, within what was clearly a storm affected US employment report released last week, the earnings data was most significant. Chart 2 below shows three separate gauges of wage growth for the US, all of which have been turning higher again in the last few months. With this backdrop, if Washington does actually pass some tax reform, and inflation starts heading higher again, how can the Fed not continue with their normalisation policy; which we think means a rate rise in December and two more in the first half of next year along with balance sheet reduction (assuming the equity market behaves).

This all points to higher yields, especially at the front end of the curve, and most likely at the long end as well.

Chart 2 – US wage growth

When it comes to the currency markets, traders and investors seem to have become very comfortable with the recent past of benign rates/yields and a perceived dovish Fed. After a near 10% decline in the Dollar, the market had become aggressively short the Dollar to the degree which is historically seen before a significant low in the level of the Dollar. Indeed, the US Dollar Index has actually risen every week for the last four weeks, and exchange data shows that speculators have barely changed their bearish positions at all. Surely this will change if the Dollar rally begins to develop some momentum?

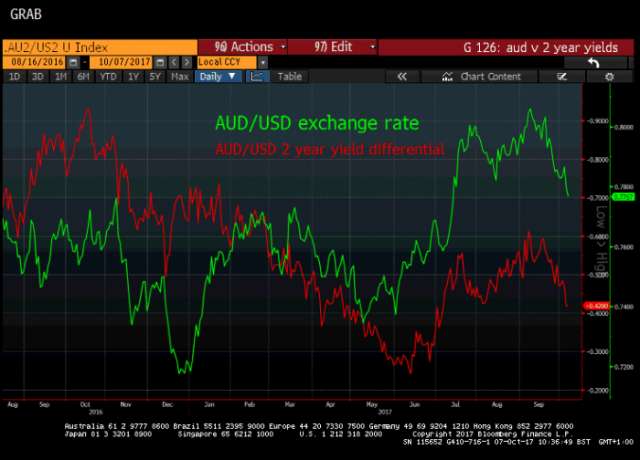

As an example of what we mean, we will look at the Australian Dollar. Chart 3 below shows the AUD/USD exchange rate (green) and the yield difference (red) between their respective 2 year bonds.

Chart 3 – AUD/USD exchange rate & 2 year yield differential

Now, if we are right that the Fed raises rates by 0.75% (or even 0.5%) between now and mid-2018, we can expect the US two year bond yield to rise by a somewhat similar amount. As for the Reserve Bank of Australia, there was no change in their policy rate at last week’s meeting, they continue to worry about any strength in the Aussie Dollar hurting their economy to the point that deputy governor Harper even hinted that the next move in rates could be down (although this view is not shared by the market that sees a 40% chance of a ¼ point rate rise by mid-2018).

Basically, we see a good chance that the yield differential will move in the US’ favour in the months ahead, perhaps by as much as 50 basis points. If this happens, we would expect the Aussie Dollar to fall against the US.

According to the CFTC data on market positioning via futures trading (admittedly a small part of the overall FX market but still indicative of market positioning a good deal of the time), speculators are holding an aggressively long position in Aussie Dollars, as seen in chart 4 below. Now although the Aussie Dollar has been trending higher for months (as most currencies have) and appeared to break above important resistance in July in the 0.7750/0.7800 area, the rally has lost momentum in recent weeks and price has fallen back to the breakout point.

In our opinion, there is a real risk that the move above resistance in July was not a proper breakout (a false breakout), and may leave the longs trapped. When we look at the actual long and short positions (in the lower panel), we can see that the longs have stopped adding to their positions in recent weeks as the Aussie has given back some ground. At the same time, shorts remain at a historically low level.

Now this may not happen immediately, but we do see the potential for the fundamentals supporting a stronger US Dollar, and if this were to occur, the drop in the Aussie could become quite a big move if the trapped longs sell out and trend followers start to sell.

Chart 4 – AUD/USD exchange rate and speculative accounts positions per CFTC data

Although we have focused on the Aussie here, that is partly because we see the chance for a decent move in rate differentials in the months ahead as the RBA stand pat. With the ECB likely to announce a QE reduction later this month, and the likes of the Bank of England and Bank of Canada promising rate rises, the outcome for these currencies may be somewhat different. However, we would note that speculative accounts are long every major currency except the Japanese Yen, and we suspect that if the Dollar does indeed rally in the months ahead, it will be quite a broad based rally.

At this point, we have to recognise that there are risks to our bullish yields and bullish US Dollar thesis. For a start, the North Korea situation is far from resolved, and as seen late on Friday, as concerns increase that North Korea does something (missile tests), the reflexive market reaction is to send both yields and the Dollar down. Our view is that these geopolitical concerns are really just a temporary if unsettling issue for markets.

Of greater concern would be not just the failure of the Trump administration to pass any sort of tax reform, but the behaviour of Trump himself. For the moment, Trump’s daily rhetoric has not worsened in the last month or so (could it get any worse?), and we think that some sort of tax legislation is simply a must for him to declare any substantive policy wins in his first year as President. We also have to acknowledge that the Fed in 2018 could be very different as a new Chair will be announced along with several new Governors. Will the new appointments be seen as dovish or hawkish? We will have to wait and see.

Overall, as we see fundamentals, market analysis and market positioning today, we think that the higher yields and stronger US Dollar thesis has a good deal of merit. What we are less sure about is whether equities, corporate bond and emerging market bonds will react. In theory, they should all suffer a negative reaction to higher yields and a stronger Dollar, but so far they have ignored what appears to be a subtle change in market character in recent weeks.

History tells us that if yields and the Dollar rise far and fast enough, emerging market assets are most at risk, and we know that investors have been flocking to emerging market assets in the last 18 months. We believe that the conditions are in place for a nasty reversal in emerging markets, but price momentum needs to shift downwards for this theory to become a reality. We are watching this space very closely, as we believe that flows into Emerging Market bond ETFs in particular are emblematic of a significant misallocation of capital, and with liquidity likely to be almost non-existent if sellers emerge in any size, price could move a lot more than many expect.

As for developed economy equity markets, well, our topping thesis has been wrong so far. The rise in headline indices has remained persistent and realised as well as implied volatility has basically been matching record low levels. Indeed, Art Cashin, Wall Street veteran of 50+ years said last week that he has never seen anything like it. Of course, the market could continue to move higher, but the fundamental valuation of the market simply reaches further and further into bubble territory.

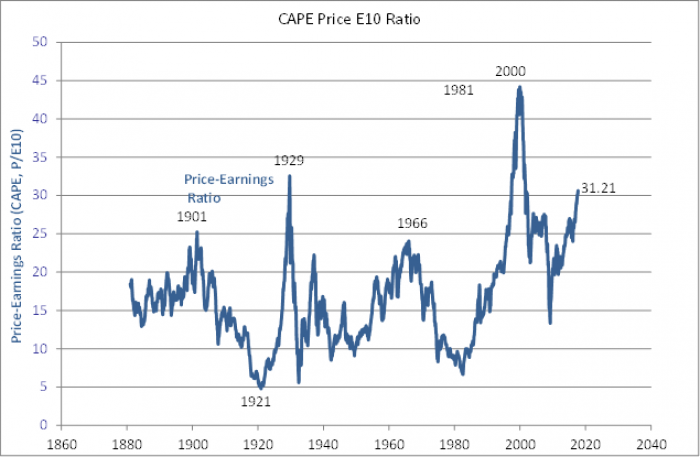

Chart 5 shows the Shiller Cyclically Adjusted PE ratio. This measure of price to earnings has only been higher about 3% of time over the last 136 years, and investors who chose to buy and hold for the subsequent 10 years during that 3% of observations were surely disappointed with the negative returns they ultimately received?

Chart 5 – Shiller CAPE chart

Many will argue that companies have become adept at using both non GAAP shenanigans and financial engineering to manipulate earnings, and price to earnings measures have their drawbacks. We agree, and although smoothing earnings as the CAPE measure does, perhaps all earnings based measures are under stating the bubble valuation that the US market has now reached. Surely all market historians accept that the 2000 peak was if not THE greatest bubble in history, then only matched by the 1929 peak, and only then because the ensuing depression was so awful.

We hear from those invested in US equities that although the market is expensive on earnings based measures, it could get even more expensive; and it could. However, on non-earnings based measures, we are either approaching the 2000 peak, or have even exceeded it. Chart 6 below shows the S&P 500 Price to Sales ratio. We like this because although companies can (and do, in some cases extensively so) manipulate earnings, it is much harder to manipulate sales. On this measure, according to the data provided by Bloomberg, the US equity market is within a few per cent of matching the most expensive valuation point ever in history, which was followed by devastating losses.

Chart 6 – S&P 500 price to revenue

So to try and conclude on our big picture thoughts as we head into the fourth quarter, we think that the ingredients are in place for a higher yield and stronger US Dollar environment. We have been calling for this for a good two months at least, and it’s been like watching a super tanker trying to slow down and change direction. As such, we have been careful in positioning for this new environment, and have been tactical in holding bullish Dollar and bearish bond positions. If price develops as we expect, we will become more confident in holding these positions.

If momentum does in fact begin to turn in risky assets, then we have to be open to the potential for the Fed and other central banks to move back to a very dovish position. However, what if employment and inflations trends are ahead of their targets as we think they will be in the first half of next year? Can they really turn that dovish just because financial markets suffer a bout of volatility and a long overdue correction? Time will tell, but we remain firmly of the view that the Fed in particular will tighten policy until something breaks, either in the real economy or the markets.

Any such break is more likely in the second half of next year, but the point is that markets will already be moving by that time and markets could be very different by the time the break is obvious. Central banks have been instrumental in creating the conditions for an “everything bubble” and investors have played their part in pushing many prices to extreme levels. If global yields do move higher in the months ahead, coincident with tighter monetary policy and a stronger Dollar, the everything bubble will become ever more vulnerable.

Stewart Richardson

RMG Wealth Management

More about:

-1780923278.jpg&h=190&w=280&zc=1&q=100)