"We can`t recall a time when a change in leadership in Washington had the potential for such large and diverging effects on the U.S. economy," Bank of America Merrill Lynch analysts said in a recent note.

Strategists are thus doing their best to hedge their calls, with JPMorgan Chase & Co.`s equity outlook saying, "Due to uncertainties, these impacts [Trump`s campaign promises] are not incorporated into our base case earnings forecast until there is more clarity around which policies will be emphasized and/or are politically feasible."

But given the market`s forward looking nature, that uncertainty hasn`t stopped a number of banks from at least trying to calculate what a Trump administration will do to their respective areas of coverage. Here are a few highlights.

U.S. Dollar

One of the biggest winners since the election has been the U.S. dollar. While many on Wall Street had been forecasting the dollar`s demise if Trump were to take the White House, the opposite has been true. Now, due to factors including the prospect for more fiscal spending and a potential tax holiday, analysts are changing their minds. Here`s a look at what some banks are saying:

- BNP Paribas SA: "We continue to be bullish on the U.S. dollar following the U.S. presidential election. The key implication of Trump’s victory is that his proposed expansionary fiscal policy is likely to push U.S. yields up and steepen the curve. As a result, USD strength has further to run, in our view, although the speed of its rise is likely to differ versus the different G10 currencies." The team adds that they are most bullish on the dollar vs the Japanese yen, with one of their models targeting a rise above 120 for the currency during 2017. It is currently trading around 115, after sitting below 105 before the election.

- Citigroup Inc.: "We`ve got euro dollar falling just below parity, as consistent with the rate differentials very much moving in favor of a weaker euro. I mean, it`s largely driven by the U.S. side of things and a changing policy mix really gets you to a stronger dollar environment."

- Bank of America Merrill Lynch: "The Trump electoral victory is likely to lead to substantial U.S. fiscal easing, helping push the U.S. dollar up and yields higher," the firm writes, adding that it expects the Euro to trade at 1.02 vs. the dollar by mid-2017 and the yen to hit 120.

Of course, there are also signs that the "long U.S. dollar" trade is getting crowded.

Bond Yields

While the vast majority of Wall Street was betting on interest rates to continue moving lower, that has not been the case. Analysts are now calling for yields to rise, marking an end to the bond bull market.

- Bank of America Merrill Lynch: "The U.S. election was a game-changing development for markets, with single-party rule likely leading to significant fiscal stimulus. We look for a stronger U.S. dollar and higher U.S. yields in 2017," the analysts write, adding that they are targeting a U.S. 10-year rate of 2.65 percent for the end of next year.

- Credit Suisse: "In our judgement, President-elect Donald Trump`s policies are stagflationary at worst, or reflationary at best. Either way, bonds face challenges."

- BNP Paribas: "The key implication of Trump’s victory is that his proposed expansionary fiscal policy is likely to push U.S. yields up and steepen the curve."

Equities

Stocks, some sectors in particular, have rallied to new highs following Trump`s win. In their outlooks for 2017, a number of analysts attempted to gauge which sectors would see the biggest boosts.

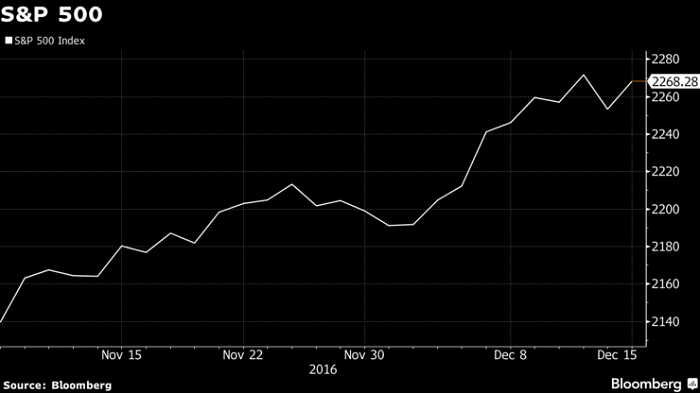

- Deutsche Bank: "If the corporate tax rate is cut to 25 percent, all else the same, it would boost S&P earnings by $10 and support an S&P rally to 2,300 and 2,400 by 2017 end."

- JPMorgan Chase & Co.: "We estimate that Trump’s corporate tax plan, which incorporates a 15 percent statutory federal tax rate, would add roughly $15 to S&P 500 earnings."

- BNP Paribas: "After lagging since 2013, U.S. small caps may face more favorable fundamental trends than their larger peers under Trump administration."

Dividends and Buybacks

- BNP Paribas: "In 2004, Congress implemented a 5.25 percent tax holiday on foreign profits for U.S. multinationals which resulted in $362 billion being brought on onshore. This led to dividend + buyback growth of +46 percent/+26 percent in 2005/2006 on top of adjusted earnings per share growth of just +12 percent/+15 percent over the same period. Markets have started to price the potential for a repatriation tax holiday as a part of corporate tax reform."

- Deutsche Bank: "If a repatriation holiday is introduced at a ~5 percent rate, as opposed to the generally proposed 5-14 percent rates, 10 percent even by Trump, then we think ~$500 billion will be repatriated in 2017. These funds will go to a combination of dividends, buybacks, onshore debt reduction, M&A and capex. We think a permanently more tax efficient means to access offshore earnings via a lower U.S. corporate tax rate, and thus lower repatriation tax, causes many S&P Tech, Health Care and Staples firms to boost their dividend payout ratios."

- JPMorgan Chase & Co.: "Cash repatriation alone could boost shareholder payouts by ~$350 billion over multiple years, with possibly even greater payouts coming from freed up cash on the back of a reduced tax rate — we estimate that buybacks from repatriation alone could add ~$1.30 to S&P 500 earnings per share, assuming that 60 percent of potential payouts come in the form of buybacks."

/The Bloomberg/

-1780923278.jpg&h=190&w=280&zc=1&q=100)